Getting your first credit card can feel a little intimidating.

Maybe you’ve heard credit cards are dangerous. Maybe you’ve heard they’re necessary to build credit. Maybe you’ve heard both from the same person.

The truth is that credit cards are neither good nor bad. They’re simply financial tools. When used responsibly, they can help you build a strong credit history and open doors to future opportunities. When used carelessly, they can become expensive debt that takes years to pay off.

Let’s break down how credit cards work and how to use them wisely from the very beginning.

What Is A Credit Card?

A credit card allows you to borrow money from a lender to make purchases.

Unlike a debit card, which uses money already in your bank account, a credit card allows you to spend now and pay later.

Each month you’ll receive a statement showing:

- Purchases you made

- Any payments you’ve made

- Interest charges (if applicable)

- Your remaining balance

If you pay the balance in full each month, you can often avoid paying interest altogether.

Why Credit Cards Matter

Many people don’t realize how important credit can be until they need it.

A strong credit history may help when:

- Renting an apartment

- Buying a vehicle

- Purchasing a home

- Qualifying for certain jobs

- Obtaining lower interest rates

Credit cards are often one of the easiest ways to begin building that history.

Your First Credit Card May Not Be Fancy

One mistake many new credit users make is comparing themselves to people who have been building credit for years.

Your first card may not have great rewards.

It may have a small credit limit.

It may even be a secured credit card or a store card.

That’s okay.

Everyone starts somewhere.

Think of your first card as a training tool rather than a status symbol.

What Is A Secured Credit Card?

A secured credit card requires a cash deposit that serves as collateral.

For example, you may deposit $300 and receive a $300 credit limit.

While that may not sound exciting, secured cards can be excellent tools for:

- Building credit

- Establishing payment history

- Learning responsible credit habits

Many people eventually graduate from secured cards to traditional credit cards after demonstrating responsible use.

☕ Kitchen Table Talk

Once upon a time, I had a not-so-fancy department store credit card.

Like many young people, nobody had really explained credit to me. The advice I received was basically, “Pay it on time or it will go on your permanent record.”

The problem was that I already had experience with something called a permanent record. I spent plenty of time in detention growing up, and nothing from that so-called permanent record seemed to affect my adult life. So naturally, I assumed this credit card permanent record wasn’t a big deal either.

I was wrong.

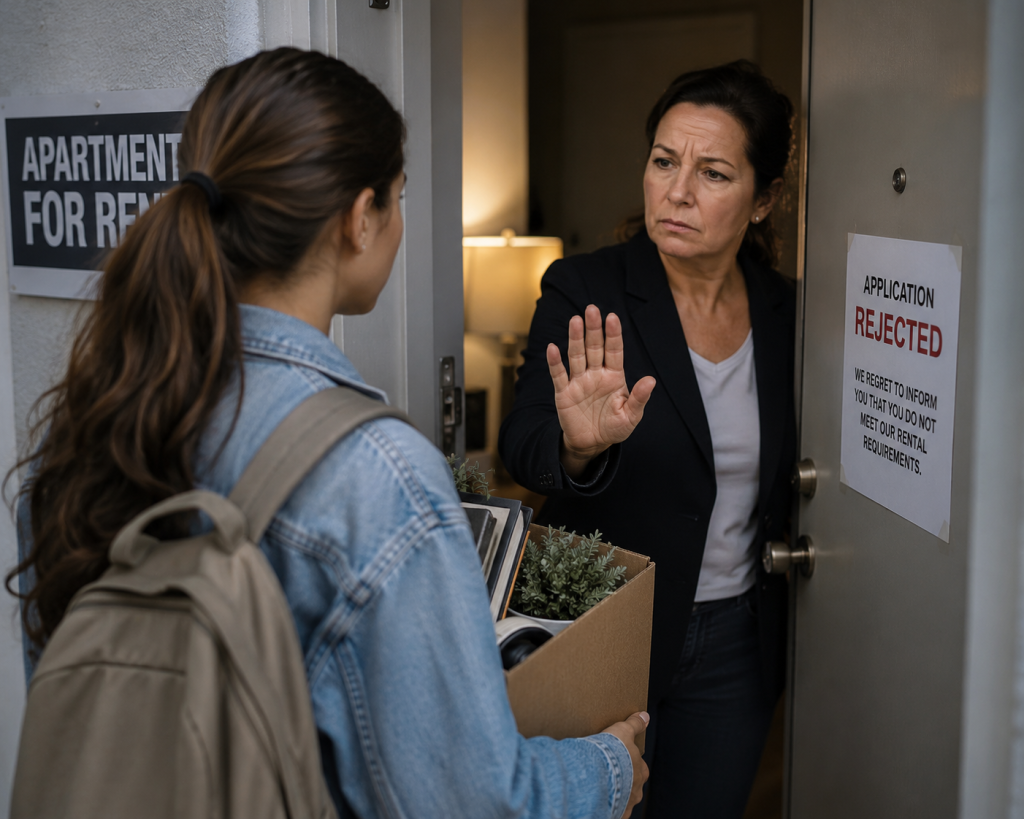

Years later, after relocating from Tennessee to Los Angeles, I needed an apartment. I didn’t have local references, family connections, or a long rental history in California. What I did have was a credit report that reflected some poor decisions I had made when I was younger.

That’s when I discovered what my real permanent record looked like.

Rejection.

Apartment applications became much harder than they needed to be. Eventually, I had to rely on a roommate with stronger credit than mine just to get my foot in the door.

That experience taught me a lesson I never forgot.

I decided to rebuild my credit the right way. One of the tools that helped me do that was a secured credit card. It wasn’t glamorous. It didn’t come with travel rewards, airport lounges, or fancy perks. But it gave me a second chance.

I kept that card for years because it represented the beginning of my credit comeback story. It also became one of the oldest accounts on my credit report, which helped strengthen my credit history over time.

The lesson?

Start building good habits from the beginning.

Pay on time.

Respect credit.

Be patient.

The cards with lower interest rates, cashback rewards, travel benefits, and premium perks often come later. Think of your first card as the training ground that helps you earn access to those opportunities.

Credit is a lot like a driver’s license. It’s a privilege, not a right. When you use it responsibly, it can open doors and create opportunities throughout your life.

The Most Important Rule: Pay On Time

If you remember only one thing from this article, remember this:

Pay every bill on time.

Payment history is one of the most important factors affecting your credit profile.

Even a single late payment can remain on your credit report for years.

Setting up automatic payments or calendar reminders can help you stay on track.

Keep Your Balances Low

Just because a card gives you a spending limit doesn’t mean you should use all of it.

A good rule of thumb is to keep your balance below 30% of your available credit limit.

For example:

If your credit limit is $1,000, mentally tell yourself your real limit is $300.

Train yourself from day one to treat that 30% amount as your spending ceiling.

By doing this, you’ll build healthy habits while helping maintain stronger credit scores.

Even better, if you can pay off 100% of that balance each month, you’ll establish a pattern of responsible credit use that lenders love to see.

It’s the little habits practiced consistently that build strong credit over time.

Understanding Debt-To-Income Ratio

As you begin using credit, it’s important to understand how debt fits into your overall financial picture.

One useful measurement is your debt-to-income ratio, often called DTI.

DTI compares your monthly debt payments to your gross monthly income.

For example:

- Monthly income: $4,000

- Monthly debt payments: $800

Debt-to-Income Ratio:

$800 ÷ $4,000 = 20%

Many financial institutions prefer to see total monthly debt obligations remain around 30% of gross monthly income.

Mortgage lending is often the exception because housing costs can represent a larger portion of income. Depending on the loan program and overall financial profile, mortgage-related debt ratios may be higher.

Understanding your DTI can help you make smarter borrowing decisions and avoid taking on more debt than you can comfortably manage.

Don’t Apply For Every Card You See

It can be tempting to apply for every credit offer that arrives in the mail.

Resist the urge.

Each application may result in a credit inquiry, and opening several new accounts in a short period can create unnecessary risk.

Choose credit products carefully and only apply when there is a clear purpose.

Credit Cards Should Support Your Goals

Every purchase you make today affects future opportunities.

Before charging a purchase, ask yourself:

- How will this affect my goal of buying a better car?

- How will this affect my ability to save for a home?

- How will this affect my retirement savings?

- Am I buying this because I need it or because it’s on sale?

Many purchases feel like bargains in the moment.

But if you carry the balance for months and pay interest along the way, that “great deal” may end up costing far more than the original price tag.

Being mindful doesn’t mean never spending money.

It means making sure today’s decisions support tomorrow’s goals.

Final Thoughts

Credit cards can be powerful tools for building a strong financial foundation when used responsibly.

Your first card doesn’t need to be perfect. It simply needs to help you establish good habits.

Focus on paying on time, keeping balances manageable, understanding how debt fits into your financial picture, and making thoughtful purchasing decisions.

Over time, those habits can help you build the kind of credit profile that supports bigger goals like buying a car, purchasing a home, and creating long-term financial stability.